by Michael Hollister

Exclusive published at Michael Hollister on June 07, 2026

7.973 words * 43 minutes readingtime

This compass is published as part of Hollister’s Geopolitics.

New analyses every week – subscribe for free.

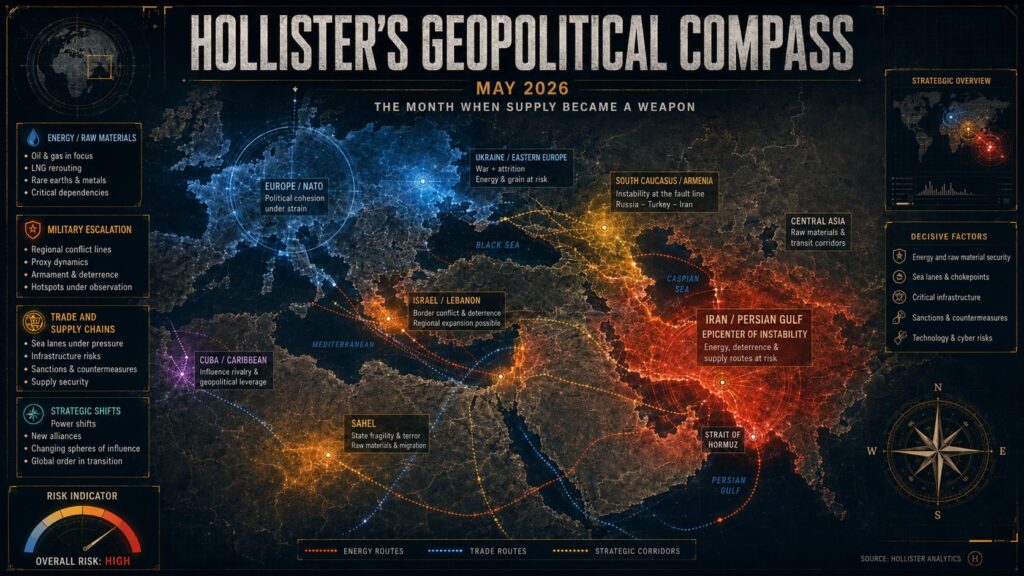

May 2026 * The Month Supply Became a Weapon

1. Monthly Diagnosis

Whoever followed the headlines in May 2026 saw half a dozen separate crises: a fragile ceasefire in the Gulf, a grinding war of attrition in Ukraine, a summit between Washington and Beijing, a collapsing front in the Sahel, and a failing island in the Caribbean. Whoever sets these events side by side sees something different – not six crises, but one movement. At its center stands not a battlefield, but a commodity: energy.

The pace is set by a clock that has been running in Washington for years. The RAND Corporation had already outlined a closing window against China in 2016 and 2017; its studies and the official National Security Strategy of November 2025 identify the decade between 2025 and 2035 as the phase in which the United States can still claim military superiority in the western Pacific. By mid-2026, Washington stands at the near edge of that window – which explains the tempo. The same strategy classifies Russia as manageable and no longer views Europe as a partner, but as a risk.

The second driver is the dollar. As long as oil and gas are traded in dollars, the world economy remains chained to the American currency – regardless of whether individual states shift their reserves into another unit of account. Whoever controls the energy market controls demand for the dollar. This is precisely where the pressure applies: while the BRICS states deliberate on a common unit of account, Washington is not securing the currency but what it is spent on. Trump articulated this logic himself in January, after the detention of the Venezuelan president, when a reporter asked what taking over a South American country had to do with “America First”: the goal was to “surround ourselves with energy.” Venezuela’s reserves, Iran’s supply routes, the chokepoints from Hormuz to Panama – in this reading they are not separate theaters, but levers of the same grip.

In May this logic became material. In the Gulf, the de facto closure of the Strait of Hormuz kept oil prices elevated and drove up the cost of fertilizer and sulfur around the globe; at the same time, the UAE’s exit from OPEC tore a split through the cartel. In the Caribbean, the same weapon – oil, this time as a blockade – pushed Cuba to the edge of collapse. In Europe, Washington announced it would reduce its military presence. In the Sahel, the Russian security model disintegrated, its weakness removing a rival the United States had considered manageable anyway. And while the world’s attention was fixed on Iran, four capitals in the Sunni world drew together into a new bloc.

Whether these moves constitute a meticulously planned campaign or a chain of opportunities pointing in the same direction is debatable – the direction itself is not. The architecture behind them I have described in greater depth in Operation Pivot. The Compass does something else. It does not ask what happened – you know that from the news – but what set it in motion: who is gaining room to maneuver, who is losing it, and which material chains are snapping in the process.

In May 2026 it became visible that power is again being decided where oil, commodities, and sea lanes converge. Let us begin where the pressure was highest – in the Gulf.

2. Hormuz: Oil, Fertilizer, and the Fracture in the Gulf

Ten weeks after the war began, the Strait of Hormuz remained de facto closed through May. The US Navy maintained the sea blockade against Iranian ports it had established on 13 April; by late May, Washington and Tehran were negotiating a memorandum that would extend the ceasefire by 60 days, reopen the strait, and end the blockade – while Israeli attacks in southern Lebanon continued to strain the truce. But the real story of the month was not in the war dispatches, but in the price tables.

On 07 April, the European benchmark North Sea Dated had beaten the previous record from 2008 at 144.68 dollars per barrel – back then it was speculation, this time a physical supply shortfall. By mid-May the price hovered around 110 dollars, more than 50 percent above pre-war levels, with daily swings the market had last seen after Russia’s invasion of Ukraine. Gulf production was 14 million barrels per day below pre-war levels according to the International Energy Agency; the global net shortfall was just under 13 million. OECD states coordinated drawdowns of their strategic reserves – and still failed to close the gap. A strait 21 miles (33 km) wide was deciding the supply of half a continent.

The first aftershock hit not the pump but the field. Around 30 percent of seaborne fertilizer trade runs through Hormuz; with the closure, prices for nitrogen and phosphate fertilizers shot up. Urea is on track for a gain of nearly 60 percent in 2026; sulfur costs – a basic input for phosphate production – have doubled. The World Fertilizer Index thereby reached its highest level since late 2022; agronomists warn that even a 10 percent drop in fertilizer application can reduce next season’s corn and wheat yields by five to eight percent. Tankers anchored in the hundreds outside the Gulf because no insurer would any longer cover the war risks; deliveries were rerouted via expensive land corridors. In India, deliveries of liquefied petroleum gas – the cooking fuel of households – fell by more than 40 percent; queues formed at bottling stations. Where fertilizer becomes scarce, bread becomes scarce a year later: the crisis migrates from the tank into the food chain, and it hits the poorest first.

The second wave reached Asia’s industry. China cut its crude imports within two months by 3.6 million barrels per day to 7.9 million – the largest drop recorded by a single country; Beijing’s petrochemical industry, the backbone of millions of jobs, ran on minimal power. Japan and South Korea throttled their naphtha processing; Pakistan, the Philippines, and Sri Lanka introduced four-day work weeks – echoes of the 2022 energy crisis. A second bottleneck appeared below the crude oil level: because refining capacity was missing globally, diesel and kerosene premiums tripled. That it was specifically China’s supply that suffered most is, in this constellation, not an operational accident but the actual thrust of the strategy.

For the same closure that was suffocating Asia lifted a new oil order out of the water. The United States became a net crude oil exporter in a single week in April for the first time in over 50 years, pumping at record levels; Brazil’s production reached its third consecutive all-time high. Venezuela, until months ago under maximum sanctions, delivered 1.12 million barrels per day in April – the highest level since 2019, after Chevron, Repsol, and Eni had expanded their stakes within two weeks. And Russia profited from the scarcity: despite Ukrainian attacks on its refineries, export revenues rose to 19.2 billion dollars in April.

Placed side by side, this forms a hierarchy, not a coincidence. Iran is the target – its oil exports fell under the blockade to around half a million barrels per day. Russia is the instrument – tolerated as a market buffer while sanctions formally remain in place. Venezuela is the replacement source – unlocked precisely at the moment the Gulf dropped out. Three decisions, one purpose: secure supply without the key rival finding an opening.

Into this shift burst a fracture in the cartel itself. On 28 April, the United Arab Emirates left OPEC after nearly 60 years, announced an investment package of 55 billion dollars, and expanded its Hormuz bypass via the port of Fujairah. OPEC production stands at its lowest level in over 35 years. When a founding member exits because production quotas are cutting into its returns – what is stopping Saudi Arabia or Iraq from doing the same the moment prices fall? Precisely this fault line has been running through the Gulf region for months.

What appears as a Gulf crisis is thus something else: the forced self-disclosure of an order that had long since shifted. The mines in the strait are not cleared, no state has taken on clearance, and without clearance there is no insurance, without insurance no tankers – the crisis will outlast whatever happens at the negotiating table by months. Even in the IEA’s most favorable scenario – a gradual reopening from June – the market remains in deficit through October; the strategic reserves once drawn down must be refilled over years. The question is therefore no longer whether the oil world is reordering itself, but who ultimately determines the winners, losers, and quiet beneficiaries.

3. Europe: Washington Steps Back, the Continent Arms Up

In May, the tone of the Ukraine war shifted in several places simultaneously – and none of them were a battlefield. At the front the situation stabilized; The Economist and the Financial Times described in late May a Ukraine “turning the tide” because mass-produced drones were braking Russian advances. Vladimir Putin stated on 09 and 29 May that the situation was approaching “completion,” without naming a timeline. Washington set a deadline for an agreement in June. But the most consequential signal came from a NATO meeting in Sweden: US Secretary of State Marco Rubio announced that the American military presence in Europe would shrink over time.

This is not the end of a war, but the European front of a larger move. The official US strategy classifies Russia as “manageable” and instructs Europe to bear the cost of its own conventional defense going forward. America is withdrawing forces and attention in order to have them free for the Pacific. Europe is left with the bill – and is beginning to pay it.

The aftershock is the fastest rearmament of the continent since the Cold War, running on three levels simultaneously. First, command: on 06 February, Europeans for the first time took over all three of NATO’s operational war commands in Norfolk, Naples, and Brunssum, while the United States retained the strategic supreme command level and the post of supreme commander. Europe will henceforth run the warfighting; America retains control over it. Alongside this, a treaty architecture is growing that Polish commentators call a “NATO within NATO”: bilateral mutual defense pacts between Poland, France, the United Kingdom, and – planned for June – Germany, explicitly built to bypass slow Alliance processes and uncertain American backing. The German-Netherlands Corps in Münster is to lead NATO land forces in the Baltic states in future, up to 60,000 troops. Prime Minister Donald Tusk explains this strategy openly: in an emergency, the goal is a rapid response from Paris and London before the Alliance has even convened – and without having to wait for Washington. Legally it remains NATO; politically, an alliance within the Alliance is emerging that does not conceal its geographic thrust.

Second, money. Germany’s defense budget rose in 2026 to 108 billion euros, a doubling within two years – made possible by a constitutional amendment that permanently exempts defense expenditure above one percent of GDP from the debt brake. “The threat situation takes precedence over the budget situation,” the defense minister put it. At the EU level, 150 billion euros in loans with maturities of up to 45 years are available for joint procurement – in which Ukraine and Canada may also participate – and the Commission speaks of up to 800 billion. Its Readiness Roadmap 2030 names four priorities: Eastern Flank Watch, a European drone defense, an air shield, and a space shield. Whoever can assign four of them to a single conceivable adversary understands against whom this architecture is being built. When a state amends its constitution to permanently decouple armaments from budget logic, that is no longer fiscal policy – it is a prejudgment.

Third, personnel. Since 01 January, all 18-year-olds in Germany receive a Bundeswehr questionnaire; the legally enshrined target is 460,000 soldiers by 2035, and a “contingency conscription” provision is activatable by a simple Bundestag resolution. In April, the Ministry of Defense presented the strategy of a “New Reserve”: 200,000 reservists are to protect critical infrastructure, secure transit routes, and serve as a buffer between the homeland and the front within the framework of the “Germany Operations Plan.” That is not an army for overseas missions, but for national defense. Armored Brigade 45 “Lithuania” – Germany’s first permanently abroad-stationed combat formation since the Second World War – is to grow to over 5,000 soldiers by end of 2027; its barracks in Rūdninkai are under construction. In the Lithuanian forest, German special forces exercised for three weeks in May a scenario in which Russia has occupied the Baltic states. The adversary is named in no official statement – it need not be.

The second major effect changes what Europe arms itself with. The war in Ukraine has made the drone the decisive weapon, and Europe is drawing the industrial consequence: Germany, France, the United Kingdom, Poland, and Sweden agreed on joint production of drones and loitering munitions with a range of 310 miles (500 km); German-Ukrainian joint ventures in drone technology followed. Ukraine thereby shifts from recipient to laboratory – a defense site whose competence Europe imports while simultaneously financing it. European armed forces are restructuring around unmanned systems – a break with the procurement logic of past decades. Where ammunition shortage was the topic two years ago, industry is gradually converting to a war economy: drone factories, special funds, defense startups.

Who gains room to maneuver in this constellation? In the short term the United States, which is freeing up resources and attention for the Pacific. Russia, which can sit out the American withdrawal and the stalemate without having to yield itself – Putin’s “completion” is also a waiting game. And the European defense industry, drowning in orders. Who loses it? Europe as a whole: it is arming up, but without the American security net that made this rearmament unnecessary for decades.

This leaves a question hanging in the air that appears in no government statement: Is this Europe’s emancipation – or its disposal, dressed up as partnership?

4. Beijing: The Summit Without Result and the Lever That Remains

On 14 and 15 May, Donald Trump and Xi Jinping met in Beijing – a summit that had been postponed from March because of the Iran war. Trump called the visit a success, but departed without a breakthrough on rare earths. What was agreed were Chinese purchases of US soybeans and Boeing aircraft, plus a return visit in September. The actual issue remained open – and that precisely is the news.

The two closing statements read as though two different summits had taken place. The White House declared that China would “address” US access to rare earths, explicitly naming yttrium, scandium, neodymium, and indium. The Chinese side mentioned rare earths not at all. The same asymmetry had already appeared after the Busan summit in October 2025 – now for the second time in succession. When one side announces a concession the other side does not even name, the concession is not one.

This is the finding of the month: rare earths are no longer a subject of negotiation but a permanent condition. The licensing regime with which Beijing brought its exports under control in April 2025 was never lifted. What was negotiated as a standstill over the toughest restrictions in October 2025 expires in November 2026 – a countdown, not a solution. Beijing thereby holds the exact counterpart to the American energy weapon: where Washington throttles China’s oil supply via sea lanes and blockades, Beijing throttles Western industry via processing.

That this is not a reflex of the current crisis is shown by the chronology. Since 2023, Beijing has tightened its export controls in several waves – first gallium and germanium, then tungsten, antimony, and graphite, finally in April 2025 seven rare earths along with the associated magnets. And already in 2010, China halted its deliveries to Japan when an island dispute escalated. The lever is proven; what is new is simply that it is no longer being put away.

The leverage is structural, not symbolic. China processes over 90 percent of the world’s rare earths and manufactures around 90 percent of high-performance magnets. The dependence runs deepest precisely where Washington can least afford it: in the defense sector. An F-35 contains around 922 pounds (418 kg) of rare earth elements; a Virginia-class submarine over 8,800 pounds (4,000 kg). According to Pentagon-adjacent data, 78 percent of US weapons systems depend on a handful of critical minerals, and 88 percent of the Defense Department’s supply chains run through Chinese intermediate steps. That is the strategic Catch-22 Pentagon analyses have long identified: the US cannot meet China in the Pacific with material it sources from China.

Who gains room to maneuver in this situation, who loses it? China gains, without doing anything – as long as it holds the processing, it sets the tempo at which the West can free itself. The Pentagon put 400 million dollars into MP Materials, the only fully integrated US producer; it produced a record quantity of neodymium-praseodymium oxide in 2025 but continues to post losses – evidence of how far an independent supply chain still is. The losers are those who demand the loudest toughness toward Beijing: US defense, whose most advanced systems cannot leave the production line without Chinese magnets, and the European auto industry, which is simultaneously shifting to electric vehicles and multiplying its mineral requirements. The AI race intensifies the pressure, for every data center expansion increases demand for exactly the elements Beijing controls.

Beijing therefore need not even pull the lever loudly. It issues general licenses while keeping the structural bottleneck closed. Even during these relaxations, heavy rare earths like dysprosium and terbium remain a bottleneck. Should the standstill expire in November without extension, the International Energy Agency estimates the risk at 6.5 trillion dollars of annual economic output outside China – the auto and electronics industries first. For Washington the timing is fatal: the same RAND logic that drives the Pacific pivot demands capability in exactly the decade when the material dependence is greatest.

The summit changed nothing, because it could not change anything. One analyst put it soberly: Beijing will say what needs to be said to keep the next few years quiet – and wait for the next US president. Rare earths are not the point on the agenda. They are the reason Washington’s entire Pacific pivot is a race against a clock that China is setting from the other end.

5. The Quiet Axis: A Bloc Forms Around an Unreliable Protector

While the West focused in April on the second round of negotiations between Washington and Tehran, a movement was taking shape in the background that barely made headlines. On 07 April, Donald Trump – 90 minutes before his own deadline – announced a ceasefire with Iran, following a phone call with Pakistan’s Prime Minister Shehbaz Sharif and Army Chief Asim Munir. Eight days later Sharif set out on a four-day journey: Riyadh, Antalya, Doha. Three capitals, three strategic partners – and a consultation movement the West dismissed as a footnote.

Pakistan had become the switching center. Already on 29 March, Islamabad had received the foreign ministers of Saudi Arabia, Egypt, and Turkey to discuss de-escalation and the reopening of the Strait of Hormuz; as mediator between Washington and Tehran, the country was carrying messages between the fronts. From this broker role something larger grew.

It concerns four capitals: Pakistan, Saudi Arabia, Turkey, and Qatar. Former Israeli Prime Minister Naftali Bennett had named the first three already in February; Qatar belongs to the movement without formally sitting at the table. The core is formed by a defense agreement that Riyadh and Islamabad signed on 17 September 2025 – an attack on one country is to be regarded as an attack on the other. This is more than a mutual defense clause: Pakistan is the only nuclear power in the Islamic world, with around 170 warheads. Across the quiet axis, barely spoken aloud, a nuclear umbrella thereby extends over the Gulf.

This bloc is forming not despite the United States, but because of them. The same withdrawal that drives Europe to rearm is prompting the Gulf states to take precautions: if Washington’s guarantee hangs on conditions, the Sunni states are building their own. On 13 May, reports densified suggesting Turkey and Qatar could formalize their place in the pact. The axis is hedging against two things simultaneously – against Iran across the water and against an America that may not come. Turkey’s role stands out: a power the West increasingly treats as a rival becomes the axis’s hinge. And even Iran cannot be neatly filed under adversary – the same Pakistan that is co-sponsoring the Sunni umbrella is simultaneously mediating for Tehran. The axis is directed less against any single country than against dependence itself.

Noteworthy is who is taking precautions. Qatar hosts Al Udeid, the largest US air base in the region – and is nonetheless sounding out a hedge beyond Washington. Reports suggest a quartet of Egypt, Pakistan, Saudi Arabia, and Turkey is even examining a joint deterrence arrangement that would not be directed solely against Iran. What is emerging here is not a NATO replica, but something looser and for that reason more robust: a fabric of bilateral pacts and consultations, Sunni-grounded, nuclear-underpinned, increasingly independent of American will. That a former Israeli head of government was first to name the movement by name shows how closely it is being registered in the region.

The connecting element remains Pakistan’s rise. For years isolated, Islamabad is now being courted simultaneously by China, the Gulf states, Iran, and the United States. India’s bet on isolating Pakistan has backfired: even while Washington on 26 May concluded a trade agreement worth 500 billion dollars with New Delhi, it kept Pakistan’s tariffs at 19 percent – against 50 percent for India. Islamabad’s value has risen, not fallen.

The Gulf is thereby slipping doubly out of Washington’s grip. In the same month the Emirates left OPEC and detached their production policy from the cartel, those same Gulf states are detaching their security from the American guarantee. Energy and defense – the two levers with which the United States bound the region for half a century – are loosening at the same moment.

All of this is happening while the United States is looking elsewhere. The logic of the pivot is concentration: withdrawal from the Middle East and from Europe, massing toward the Indo-Pacific and China. The Gulf bloc is the foreseeable echo – tenants build their own roof when the landlord announces a move. While a new bloc is forming in the Gulf, the United States is directing doctrine and resources toward the Indo-Pacific – where, in its view, the real race is being run. What looks like emancipation in the Middle East is elsewhere the flip side of the same shift.

A nuclear-underpinned Sunni axis, sounded out in months, under an American umbrella that is just folding – that is the encirclement, seen from within. Washington is not drawing the lines here; it is withdrawing, and others are filling the space.

6. Sahel: Russia’s Model Collapses, and Africa Burns in the Shadows

Since 25 April a coordinated offensive by Tuareg rebels of the FLA and the al-Qaeda-affiliated JNIM rolled across northern Mali. Kidal and Gao fell, garrisons were overrun in several cities, and in Kati Defense Minister Sadio Camara – a key figure of the junta – died in a car bombing. But the image that summarizes the month comes from Kidal: around 400 fighters of the Russian Africa Corps negotiated an evacuation corridor and were escorted out of the city by the very rebels they had come to fight. The Mali soldiers left behind fell into captivity.

This is more than a lost city. It is the collapse of a model. The Africa Corps, successor to the Wagner Group, was the security guarantee of the junta after it had expelled France and the UN mission from the country. May showed that this guarantee is hollow: Kidal, recaptured in November 2023 with Wagner support, fell again after thirty months. It was the most coordinated insurgency offensive since the collapse of northern Mali in 2012, reinforced from 28 April by the Sahel affiliate of the Islamic State. The Africa Corps reportedly maintained ten to twelve thousand fighters in the country – and still could not hold the north. The damage radiates outward, for Russia’s position in Burkina Faso and Niger rests on the same promise: mercenaries in exchange for raw materials and loyalty, security where the West had failed. If this promise does not hold in Mali, the whole African advance of Moscow wobbles. Mali burns, Russia bleeds.

The upheaval brings no stability. The junta had expelled the West in the name of sovereignty and delivered itself into dependence on Moscow; now, as even that is crumbling, it is seeking new protectors in Ankara, Tehran, and Beijing, while the alliance of jihadists and Tuareg consolidates the north. The alliance of Tuareg and jihadists is not aiming at the conquest of all of Mali, but at dominating the north and forcing conditions in Bamako that it can steer. The multipolar competition for Africa thereby merely changes the flags on the pickups; the state itself continues to disintegrate – and in Ouagadougou and Niamey, everyone is watching closely.

Over 600 miles (1,000 km) to the east the same logic runs more lethally. After three years of war, Sudan is the world’s most severe humanitarian catastrophe: over 40,000 dead, more than 14 million displaced, confirmed famine in El Fasher and Kadugli. After the fall of El Fasher in October – an eighteen-month siege with massacres that brought the International Criminal Court into play – the Rapid Support Forces now control Darfur and the greater part of Kordofan. The besieged cities of Kordofan are the new front, and famine moves with it. The war has triggered the world’s largest displacement crisis; according to UN figures around half the population is threatened by hunger, and the fall of El Fasher drove hundreds of thousands into already overwhelmed neighboring locations.

Sudan is in this a proxy war of the Gulf powers. The Sudanese army flies Turkish Baykar drones; the RSF deploys Chinese drones widely assessed as having come from the United Arab Emirates. The same Gulf rivalries that elsewhere are drawing together into a quiet axis are killing here through proxies. Even the mediation attempt bears the signature of the same actors: a “Quad” of the United States, Saudi Arabia, Egypt, and the UAE wrestled over a three-month ceasefire – and the warring parties fought on.

The decisive point, however: almost no one is watching. At the start of 2026, diplomatic attention shifted almost entirely to the Iran war. Energy, headlines, and mediators directed themselves toward the Gulf – and in the shadow it cast, two African catastrophes deepened almost unobserved. This is the most invisible aftershock of the month: where attention and resources concentrate on one point, the rest of the board falls into darkness. Russia loses a strategic position in Mali without it being widely registered; in Sudan tens of thousands are dying in a war Gulf powers are co-financing and about which the world public reads past. Whoever sets the situation report from Mali alongside the dispatches from the Gulf sees two halves of the same shift.

Who gains room to maneuver when the major powers look away? The local militias, the proxy financiers, the warlords. Who loses it? Tens of millions of civilians – and a continent that becomes a playing board for everyone else while the world looks in a different direction.

7. Monroe 2.0: Washington Turns the Energy Weapon Inward

On 20 May, the US Department of Justice indicted Raúl Castro – 94 years old, at the time of the act Minister of Defense – over the shooting down of two civilian aircraft of the exile group Brothers to the Rescue in 1996. The charge is three decades old; the message lies in the timing. The indictment gives Washington a pretext for exactly the kind of operation with which the United States in January deposed the Venezuelan president Maduro in Caracas.

For since the seizure of Venezuela and its oil, Washington has imposed a blockade that is cutting Cuba off from fuel – an island that depended almost entirely on Venezuelan crude. The consequences are drastic: the power grid collapsed several times nationwide, in one total outage around ten million people were in the dark, water and food supply were thrown into disarray, hospitals, schools, and food production were affected. On the streets, calls for light became calls against the government; barricades burned. Cuba is being starved into a “deal” – or, as Trump put it, a “friendly takeover.”

The escalation has two hands. While the Castro indictment increases the pressure, CIA Director Ratcliffe traveled to Havana – the highest-level meeting between the two states since the start of the blockade. Coercion and offer of talks, the same fist in the same month.

This is the energy weapon from the first chapter of this issue, turned inward. Where Washington closed the Strait of Hormuz to foreign rivals, it is turning off the tap for a neighbor. Oil is the lever, the hemisphere is the lock – the Monroe Doctrine in a new edition: the continent as backyard, secured not by gunboats but by supply control. The precedent had been set by Venezuela in January.

The same logic runs through Panama. There Washington pushed to displace Chinese operators from the Canal’s ports – through which a substantial portion of US trade flows and whose Chinese concessions Washington regarded as a strategic entry point. The backyard is simultaneously being cleared of foreign footholds and the chokepoint secured. Energy, chokepoints, zones of influence: three levers, one objective.

The method repeats itself, only the pretexts change: in Mexico, cartels were declared terrorist organizations and thereby a possible pretext for interventions; in Venezuela the drug war served this purpose; in Cuba a 1996 shoot-down. And behind the oil stands a second motive. Whoever controls the hemisphere’s energy flows simultaneously secures the dollar in which this oil is traded globally. The Monroe Doctrine in its new edition is therefore also a defense line of American currency power – against precisely the de-dollarization that states like China and Russia are advancing.

Who gains room to maneuver in this? The United States, securing for itself an energy-guaranteed hemisphere cleared of Chinese influence; Venezuela’s oil flows under American control. Who loses it? The sovereignty of the states being targeted – and any external power that wanted a foot in the door here.

A president abducted in Caracas; a patriarch indicted in Miami; an island in the dark – redrawn by the same instrument that an ocean away closed a strait. The doctrine is two hundred years old, the method new. Open is only the next name.

8. Overall Assessment: Whoever Holds the Chokepoint Holds the Space

Six theaters, one pattern. What connects May is not a common actor but a common instrument: control over material flows. Oil through a strait, fertilizer by sea, rare earths through Chinese processing, fuel to an island, mercenaries for a junta – everywhere the decision was made not by firepower but by access to a bottleneck. Supply became a weapon, and whoever holds the chokepoint holds the space.

The winners of the month sit at precisely these bottlenecks. The United States leads: energy-secured in its own basin, relieved in Europe, capable of enforcement in its own backyard, with an unobstructed view toward the Pacific. In its wake, the suppliers of the new Atlantic order profit – Brazil at production records, a re-opened Venezuela under American control, the Emirates as a reliable producer outside the cartel. China wins without moving: its processing supremacy in rare earths is a pledge it need not even draw. Russia profits quietly from expensive oil, even as it loses a strategic position in Mali. And below the major powers, defense industries drowning in orders profit, as do local armed groups staking out terrain in the vacuums of disintegrating states. Yet no victory here is fully secure: America’s energy power rests on a flank controlled by Beijing, and China’s pledge depreciates to the extent the West rebuilds its supply chains. The winners of the month are winners for now.

The losers are those who hang at the end of a supply chain without controlling it. Asia’s energy-hungry industry – China’s petrochemicals, Japan’s and South Korea’s refineries – pays the price of the Hormuz closure. The poorest pay it twice, because expensive fertilizer returns a year later as expensive bread. Iran, the actual addressee of the blockade, sees its exports choked. Europe is arming up, but without the net that made this rearmament unnecessary for decades. And at the bottom of the balance sheet stand the civilians in Sudan and Cuba, whose mere supply has been turned into a pressure instrument against their governments. A quiet loser is moreover the old order of the Gulf itself: with the Emirates’ OPEC exit and the forming Sunni axis, energy and security bonds that held for half a century are both loosening.

The greatest vulnerability of the month carries a date: November 2026. That is when the standstill over China’s toughest export controls expires. If it tears, economic output in the trillions is at stake according to IEA estimates – and Washington faces its fundamental dilemma: it cannot meet China in the Pacific with material that comes from China. The second open flank is Hormuz itself. As long as the mines are not cleared, a strait 21 miles (33 km) wide can hold half the world economy hostage – regardless of what is decided at the negotiating table.

The sharpest lever is therefore not a weapon, but a bottleneck. The Strait of Hormuz, Chinese magnet manufacturing, the fuel tap turned off in front of Cuba, the sea lanes on which Pakistan’s mediation and Beijing’s ports hang – everywhere power lies where a flow narrows to a single passage. This is the sober lesson of the month: in the 21st century, war is no longer conducted only with armies but with valves. Whoever can close one needs no front. And the levers point in both directions: Washington holds the sea lanes through which China’s oil comes; Beijing holds the processing without which Washington’s most advanced weapons cannot be built. Two superpowers, each with one hand at the throat of the other – that is the statics on which this month rests.

The blind spot lies not in a region, but in perception. While attention and resources bundled around the Gulf, Africa disappeared from view – Russia’s defeat in Mali, the bleeding of Sudan. Yet the real blind spot is the pattern itself. Each of these events was reported individually, as a crisis in its own right. Set side by side, however, they reveal an architecture: the same logic in Caracas, in Kidal, at the Strait of Hormuz, and in Beijing. Whoever reads only the individual dispatch sees chaos. Whoever overlays them sees method.

The order of 1945 does not end with a bang, but with a resorting along material chains. Energy, critical raw materials, food, transport routes – these are the lines along which power is being redistributed in 2026. Reading this Compass means doing precisely that: not following the loud individual dispatch, but seeing the quiet pattern behind it. Whoever has recognized it reads the next headline differently. And the question the month poses to everyone remains sober and uncomfortable in equal measure: At which chokepoint do I hang – and who holds it?

9. Strategic Outlook: Seven Signals for the Weeks Ahead

This section is reserved for supporting readers.

A compass does not only show where you stand, but where the needle is pointing. The following seven signals are not predictions, but observation points: concrete, verifiable events at which it will be decided in the coming weeks whether the pattern of the month is solidifying or breaking. Whoever knows them reads the headlines of June not as coincidence but as confirmation or refutation of a thesis.

“Strategic Outlook” is an exclusive Chapter for Supporter

Readers who support my work will receive this article exclusively as a PDF by email on the day of publication.

If you support my work after publication and would also like to read the article, simply send a short message to:

mh@michael-hollister.com

I will be happy to send you the PDF afterwards.

Further Reading: The Compass Archive

The Compass shows the pattern. The following in-depth analyses show the evidence. Whoever wishes to follow any finding of this month back to the primary sources will find the matching long-form version here – organized by the theaters of this edition.

The Big Picture

- Operation Pivot – The master plan behind oil, chokepoints, and de-dollarization: why Trump’s policy is not chaos, but method.

- From the RAND Study to the National Security Strategy – How a think tank defined the “window” against China and Washington is implementing it word for word.

Gulf, Oil, and Food

- Who Profits from the War in the Gulf? – The new oil order, read from the IEA report: winners, losers, and the Atlantic Basin rotation.

- Follow the Oil – How Washington Is Dismantling China’s Energy Supply (Part 1) – The operational logic behind Syria, Venezuela, Iran, Panama.

- Follow the Oil – Part 3: The Gulf States Between the Fronts – Why Trump is splitting Gulf cohesion.

Europe Arms Up

- The Pattern Is Tightening – Six months in which Europe was rebuilt from peacetime to wartime mode.

- Crisis Scenario 2026 – How German industry is being prepared for a war economy.

China and the Raw Materials Weapon

- The US Materials Paradox – Washington’s Catch-22: having to act militarily with material that comes from China.

- China – The Silent Maneuver – Beijing’s calculus while the United States is expending munitions in the Persian Gulf.

The Quiet Axis

- The Quiet Axis – Four capitals, one movement: Pakistan, Saudi Arabia, Turkey, and Qatar are sounding out their own security architecture.

- The Encirclement – How a bloc is forming around the unreliable protector USA.

Sahel

- Mali Burns, Russia Bleeds – The collapse of Russia’s mercenary model in northern Mali.

- Mali Situation Report of 29 May 2026 – Current status after the fall of Kidal.

Monroe 2.0 / The Hemisphere

- Venezuela: Breaking Democracy – The precedent: the military abduction of a sitting president and the end of the rules-based order.

Aboout the Autor

Michael Hollister

is a geopolitical analyst and investigative journalist. He served six years in the German military, including peacekeeping deployments in the Balkans (SFOR, KFOR), followed by 14 years in IT security management. His analysis draws on primary sources to examine European militarization, Western intervention policy, and shifting power dynamics across Asia. A particular focus of his work lies in Southeast Asia, where he investigates strategic dependencies, spheres of influence, and security architectures. Hollister combines operational insider perspective with uncompromising systemic critique – beyond opinion journalism. His work appears on his bilingual website (German/English) www.michael-hollister.com and in investigative outlets across the German-speaking world and the Anglosphere.

Sources

The following references document the external primary data processed in the Compass. The further source landscape for the interpretive lines can be found in the linked analyses.

Hormuz: Oil, Fertilizer, and the Fracture in the Gulf

- IEA – Oil Market Report, May 2026 (North Sea Dated price spike, strategic reserve drawdown due to Hormuz disruptions). https://www.iea.org/reports/oil-market-report-may-2026 (partly paywalled)

- Euronews – UAE Leaves OPEC After 59 Years, 29 April 2026. https://www.euronews.com/business/2026/04/29/oil-prices-rise-despite-uae-exit-from-opec-as-iran-war-ceasefire-hangs-in-balance

- World Bank Blogs – Fertilizer Price Surge from Hormuz Closure (urea +60%), April 2026. https://blogs.worldbank.org/en/opendata/fertilizer-prices-surge-as-strait-of-hormuz-disruptions-tighten-

- CNBC – Fertilizer Prices and Food Security in the Iran War, 25 March 2026. https://www.cnbc.com/2026/03/25/fertilizer-price-iran-war-food-security-inflation-urea-potash-nitrogen-farmers.html

- Food Security Portal (IFPRI) – Hormuz and a Third of Seaborne Fertilizer Trade, May 2026. https://www.foodsecurityportal.org/node/3890

Europe: Washington Steps Back, the Continent Arms Up

- NATO – Europeans Take Over All Three Joint Force Commands, 06 February 2026. https://www.nato.int/en/news-and-events/articles/news/2026/02/06/european-allies-to-take-on-new-leadership-roles-in-natos-command-structure

- RFE/RL – Rubio in Sweden: US Presence in Europe to Shrink, May 2026. https://www.rferl.org/a/rubio-nato-europe-rutte-troops-summit/33762824.html

- Atlas Institute – Germany’s Defense Budget 2026 Above 108.2 Billion Euros, December 2025. https://atlasinstitute.org/germanys-path-to-kriegstuchtigkeit-the-2026-defence-budget/

- RFE/RL – EU Approves SAFE Fund of 150 Billion Euros, 27 May 2025. https://www.globalsecurity.org/military/library/news/2025/05/mil-250527-rferl01.htm

- The Irish Times – Ukraine’s Drone Power Shifts the Balance of Forces, 31 May 2026. https://www.irishtimes.com/world/europe/2026/05/31/ukraines-ramped-up-drone-power-is-transforming-its-fortunes-against-russia/

Beijing: The Summit Without Result and the Lever That Remains

- MINING.COM – Trump Leaves Beijing With No Rare Earth Deal Confirmed, May 2026. https://www.mining.com/trump-leaves-beijing-with-no-rare-earth-deal-confirmed/

- CNBC – Asymmetric Summit Balance: China Does Not Mention Rare Earths, 18 May 2026. https://www.cnbc.com/2026/05/18/us-china-announce-deals-after-trump-xi-summit.html

- E&E News / POLITICO – Busan Rare Earths Agreement Expires in November, May 2026. https://www.eenews.net/articles/trump-xi-meeting-could-shape-rare-earths-deal/

- Council on Foreign Relations – On the Asymmetry of Export Controls After the Summit, May 2026. https://www.cfr.org/event/media-briefing-making-sense-of-the-trump-xi-summit

The Quiet Axis

- Strategic Mutual Defence Agreement (Wikipedia entry; pact signed 17 September 2025 in Riyadh). https://en.wikipedia.org/wiki/Strategic_Mutual_Defence_Agreement

- Bloomberg – Pakistan Signals Turkey and Qatar May Join Saudi Defense Pact, 13 May 2026. https://www.bloomberg.com/news/articles/2026-05-13/pakistan-signals-turkey-qatar-may-join-saudi-defense-pact (paywalled)

- Arab News – Turkey and Qatar Could Join Saudi-Pakistani Pact, May 2026. https://www.arabnews.com/node/2643393/pakistan

- The Times of Israel – Turkey “Very Likely” in Pact; Pakistan’s Nuclear Arsenal, January 2026. https://www.timesofisrael.com/turkey-said-very-likely-to-join-saudi-arabia-pakistan-mutual-defense-pact/

- Chatham House – Ankara’s Hedging Strategy and the Pact, January 2026. https://www.chathamhouse.org/2026/01/talk-turkish-military-alliance-saudi-arabia-and-pakistan-reflects-ankaras-opportunistic

Sahel

- CNN – Africa Corps Escorted Out of Kidal in Humiliation, Russia’s Grip Weakens, 10 May 2026. https://www.cnn.com/2026/05/10/africa/putin-africa-corps-kidal-mali-intl-cmd

- ICCT – Causes and Consequences of the 25 April Offensive in Mali, May 2026. https://icct.nl/publication/mali-what-were-reasons-and-consequences-25-april-attacks

- The Soufan Center – The Limits of the Russian Africa Corps in Mali, 12 May 2026. https://thesoufancenter.org/intelbrief-2026-may-12/

- UN News – “No Corner of Sudan Is Safe”: Famine and Atrocities, February 2026. https://news.un.org/en/story/2026/02/1167003

- NPR – Sudan in Its Fourth Year of War, World’s Largest Humanitarian Crisis, 15 April 2026. https://www.npr.org/2026/04/15/nx-s1-5781032/sudan-darfur-war-genocide-famine

Monroe 2.0: Washington Turns the Energy Weapon Inward

- CNN – US Indictment of Raúl Castro Over 1996 Shoot-Down, 20 May 2026. https://www.cnn.com/2026/05/20/politics/live-news/raul-castro-doj-indictment

- PBS News / AP – Indictment and Fuel Blockade After Maduro’s Fall, 20 May 2026. https://www.pbs.org/newshour/world/watch-live-u-s-expected-to-announce-indictment-of-former-cuban-president-raul-castro

- PBS News / AP – Nationwide Power Outage in Cuba Under US Energy Blockade, March 2026. https://www.pbs.org/newshour/amp/world/cuba-reports-island-wide-blackout-as-country-struggles-with-energy-crisis

- Al Jazeera – Cuba Under Oil Blockade, Trump’s Takeover Threat, 22 March 2026. https://www.aljazeera.com/news/2026/3/22/emerging-from-latest-blackout-cuba-says-ready-for-any-potential-us-attack

© Michael Hollister – All rights reserved. The distribution, publication or use of this text requires the express written permission of the author. If interested in reuse, please contact the author via www.michael-hollister.com.

Newsletter

🇩🇪 Deutsch: Verstehen Sie geopolitische Zusammenhänge durch Primärquellen, historische Parallelen und dokumentierte Machtstrukturen. Monatlich, zweisprachig (DE/EN).

🇬🇧 English: Understand geopolitical contexts through primary sources, historical patterns, and documented power structures. Monthly, bilingual (DE/EN).